(Image via

(Image viaLeaving school brings a wave of excitement as new possibilities and responsibilities await. Along with the thrill of this transition comes the important task of taking charge of your finances. Learning to handle debt wisely from the start helps you avoid common pitfalls and builds a solid foundation for your future. By paying attention to your spending and making informed decisions about loans or credit cards, you give yourself the best chance to enjoy both independence and stability. Starting on the right financial foot after graduation can shape your choices for years to come and support your personal goals.

Assessing Your Debt Situation

Before you plan your next move, it’s important to understand where you stand. Begin by gathering all your debts so you can see the complete picture. This includes student loans, credit cards, and any other bills that you may have noticed piling up over time.

Consider the following steps to evaluate your debt situation:

- List all debts with the corresponding amounts and interest rates.

- Determine the minimum monthly payment for each debt.

- Identify the debts with the highest rates, as paying those off first can save you money over time.

- Review your payment history to see if any adjustments are necessary.

By assessing your situation clearly, you build a strong foundation to plan your repayment tactics effectively. Knowing the exact numbers removes uncertainty and gives you the confidence to make informed decisions.

Creating a Realistic Budget

Designing a budget helps you see your income and expenses at a glance. Start by listing your total earnings and then subtract essential costs such as rent, utilities, and groceries. This process gives you a clear idea of how much money remains for tackling debt.

Organize your expenses into fixed costs and variable costs. Setting spending limits for non-essential items helps you avoid overspending. A realistic budget isn’t about strict deprivation; it’s about understanding what you have and using it wisely to secure your future.

Exploring Repayment Options

Different types of repayment plans address various financial situations. Research options that match your immediate cash flow and long-term goals. A tailored plan can help you clear minor debts quickly while managing larger ones over a longer timeframe.

Consider these options when evaluating repayment choices:

- Refinancing loans to lower interest rates can reduce your monthly payment obligations.

- Consolidating debts into a single payment might simplify your finances.

- Exploring income-driven repayment plans can provide relief during periods of low earnings.

- Talking to your creditors can lead to adjustments that suit your current situation.

Taking the time to explore these repayment avenues lets you match your plan with your real-life needs. This approach can offer not only financial relief but also a roadmap to a more secure economic future.

Increasing Your Income Streams

Boosting your income can give you extra funds to chip away at your debt. Sometimes a side hustle or part-time gig bridges the gap between what you earn and what you need to complete your debt payments. Trying new sources of income may introduce refreshing challenges and skills to your repertoire.

For example, consider finding freelance work, tutoring, or even participating in local projects. Remember, when you learn how to Reduce Debt, you build habits that can make a serious difference in your overall financial health. Exploring these avenues can add flexibility to your budget and reduce stress over time.

Cutting Unnecessary Expenses

Taking a close look at daily spending habits often reveals patterns that can be trimmed. Over time, subscriptions add up and small indulgences can strain your wallet. It’s about smart decisions that keep you on track without feeling deprived.

Start by identifying activities and products that don’t add long-term value. Swap expensive outings for cost-effective alternatives, like potluck gatherings instead of pricey dinners out. Even minor changes can lead to more funds being freed up to pay down your debt.

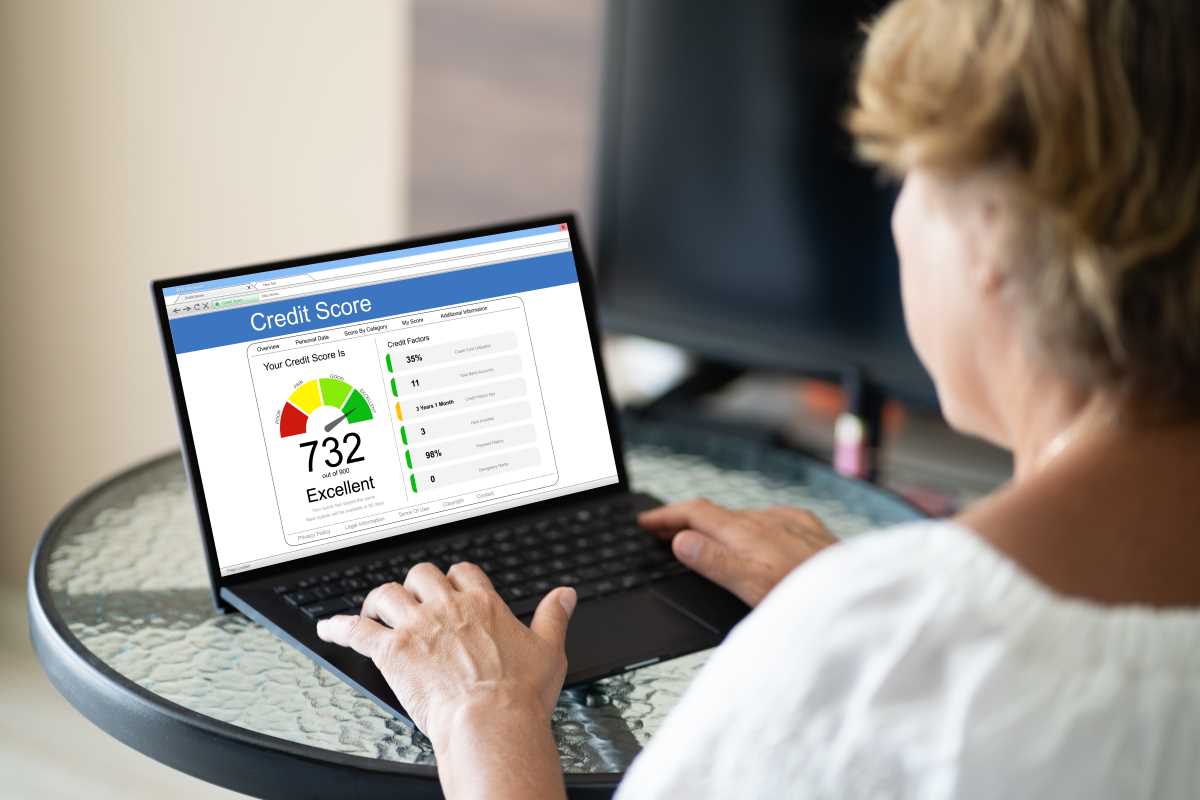

Building Good Credit Habits

Maintaining a healthy credit history is key as you manage various financial responsibilities. Consistent, on-time payments reflect well on your report and help secure better terms in the future. Making an effort to keep track of due dates and balances can make a notable difference.

Create reminders or set up automatic payments to handle bills promptly. Over time, these habits build up and demonstrate reliability. A solid credit profile stands as both a safety net and an asset when pursuing larger financial endeavors later on.

Your journey toward financial stability involves creating a plan that fits your lifestyle and future goals. With a step-by-step approach, the process becomes manageable and even empowering.

Build a solid foundation now to ensure a more secure and successful future.