Big changes such as relocating, finishing college, or switching jobs often bring unexpected challenges, including setbacks to your credit score. Even if you feel like you are starting over, you can rebuild your credit and regain your financial confidence. This guide offers simple, easy-to-follow steps to help you understand your current credit standing, pay down your debts, and adopt practical routines that steadily improve your score. You will find a clear plan that fits into a busy lifestyle without getting lost in complicated financial language. Take the first step toward a stronger credit future by exploring these straightforward tips and tools.

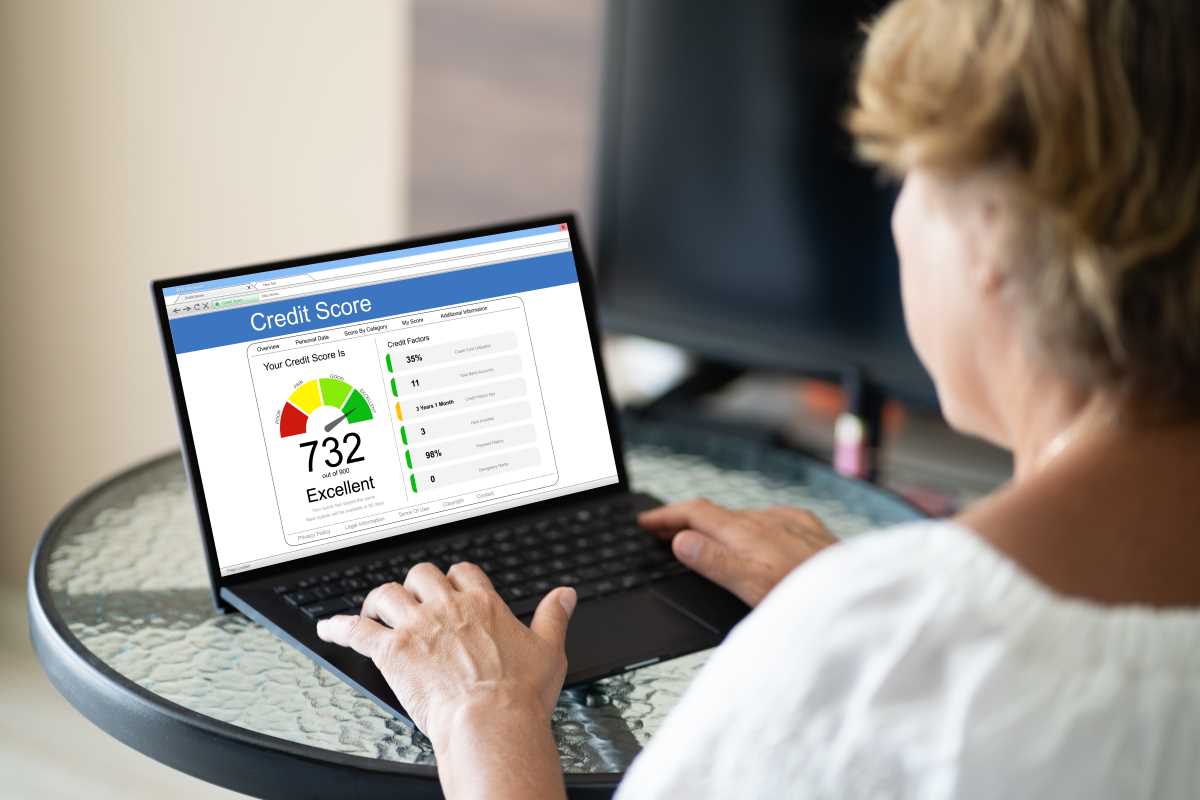

Assess Your Current Credit Profile

- Check your credit reports: Request a free copy from each major bureau. Look for errors, outdated accounts, or unfamiliar charges.

- Review your credit scores: Use free tools or banking apps that show your score. Note which scoring model they use, like FICO or VantageScore.

- Identify negative items: Highlight late payments, collection accounts, or accounts in default and mark the dates.

- Calculate your credit utilization: Divide your total balances by your credit limits; aim to keep this ratio below 30%.

Getting a clear snapshot helps you choose the right next move. If you find incorrect information, dispute it immediately with the reporting agency. Fixing mistakes can boost your score faster than any repayment plan.

Build Steady Income and Employment History

When lenders review your credit file, they examine how reliably you earn money. Securing a stable job or steady side gig demonstrates your ability to handle monthly payments. If you recently changed fields or took time off, gather pay stubs, income statements, or tax documents to show your earnings. Keep these records handy for any loan application or credit review.

If your main income stream isn’t fully dependable yet, consider adding a small part-time role or freelance work. Online platforms or neighborhood gigs can supplement your cash flow. Even a modest, consistent income can reassure lenders you’ll meet payments without trouble.

Pay Down Existing Debt Strategically

- List debts by interest rate: Put high-rate balances at the top to tackle first.

- Set a monthly payoff goal: Decide how much extra money you can put toward debts beyond minimum payments.

- Use the “avalanche” or “snowball” method: Focus on high-interest or smallest balances in sequence.

- Transfer balances if possible: Move them to a lower-rate card, but watch out for fees and terms.

- Track your progress weekly: Update your list and celebrate each time you eliminate a balance.

Paying off debts prevents interest from growing and reduces your credit utilization ratio. When you pay off one account, apply that payment to the next target. Building momentum keeps your motivation high.

Create a Habit of Making Payments on Time

Payment history forms a large part of most credit scores. Even one late payment can lower your score, so set up reminders or automatic transfers. Connect your due dates to your payday schedule to ensure funds clear on time.

If a due date conflicts with irregular income, ask your creditor about changing it. Many card issuers will adjust your billing cycle. Staying current on small balances helps you develop a reliable routine that credit agencies appreciate.

Mix Different Types of Credit

Different kinds of credit—like installment loans and revolving accounts—show lenders you can manage various obligations. If you only have one credit card, consider taking out a small personal loan or getting a secured card to expand your profile. Keep new accounts to a minimum and avoid chasing every offer.

If you’re self-employed or work freelance, you might need specialized guidance.

Monitor Your Progress Regularly

Perform a simple monthly check: note your current score, compare balances, and observe any changes in your utilization. Detecting dips early allows you to correct your course before they turn into larger setbacks. Most banks and credit apps let you view your score for free without harming it.

If you notice a sudden drop, review your recent actions: Did you close an old account? Did one bill pass its due date? Fixing small issues quickly keeps your overall progress steady and moving forward.

Paying on time, managing balances, and diversifying accounts improve your credit score. Review your profile regularly and set clear goals. Stay patient and consistent to see your score recover.